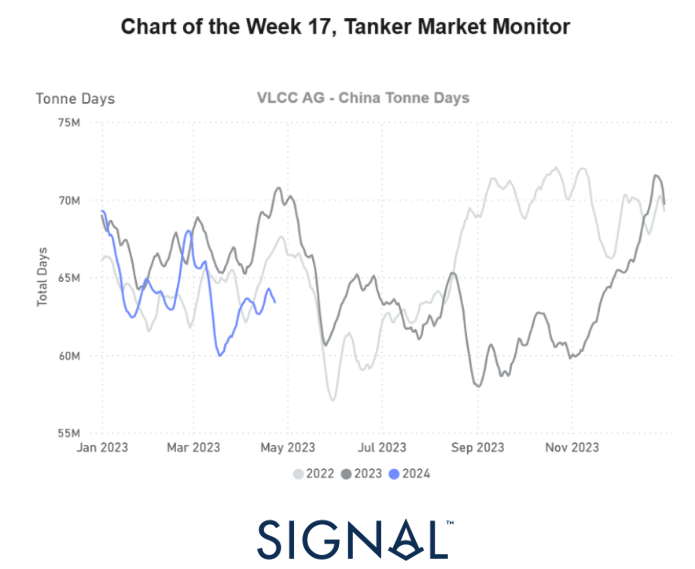

A downward revision in the growth of VLCC tonne days from AG to the Far East from March onwards

As April draws to a close, the crude freight market sentiment for VLCC and Suezmax tankers segments confirms a downward trajectory, contrasting with a sense of stability observed in the Aframax Med route, albeit accompanied by a decline in vessel activity. Turning to the demand side, the outlook for both dirty and clean tanker vessel sizes paints a challenging picture for the upcoming days of May. A clear downward trend is evident, poised to exert pressure on market prices, while signals of increased supply further compound the situation.

A closer look at the AG-China route reveals an interesting observation: the growth of VLCC tonne days recorded from March onwards is notably lower than the performance seen two years ago during a comparable period. Moreover, unlike the stable dry bulk shipping market, recent growth in tankers appears highly unlikely to reach the peak recorded in May of last year.. Meanwhile, the International Energy Agency (IEA) projects a moderate global oil demand growth of 1.1 million barrels per day (mbd) for 2025, slightly below the 1.2 mbd anticipated for 2024. Noteworthy is the significant demand growth anticipated in India, other developing Asian economies, and the Middle East. In contrast, OECD demand is forecasted to decline slightly, with European consumption easing as economic conditions improve.

SECTION 1/ FREIGHT

Market Rates (WS)

‘Dirty’ WS - Weaker VLCC - Suezmax - Aframax

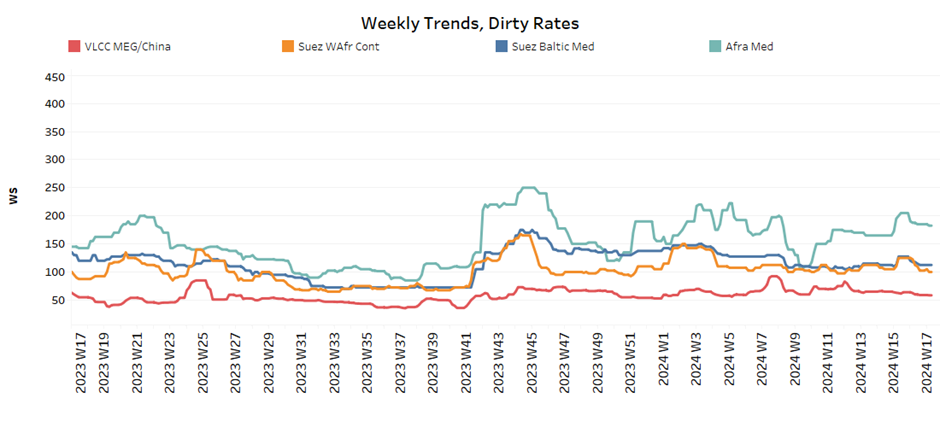

In the waning days of April, there's a discernible shift in the sentiment surrounding crude oil freight market trends. Notably, there's a consistent downward pressure observed on the VLCC MEG-China route.

The VLCC MEG-China freight rates have plummeted below 60WS, indicating a significant 12% monthly decrease compared to a similar week in February. The market's prospects for rebounding to the highs of 70WS observed in mid-February appear increasingly challenging.

Suezmax freight rates for shipments originating from West Africa to continental Europe have maintained a level around 100WS, indicating a similar momentum of a month ago. In the Suez Baltic Med route, rates are now standing below 120WS, almost 5% higher than a month ago.

Aframax Med freight rates have surged to an impressive xs 180 WS, showcasing a remarkable 27% rise compared to the same week last year. Notably, these recent levels stand considerably higher than the lows of 110WS recorded in early March, underlining a notable upward trajectory in the market.

‘Product’ WS

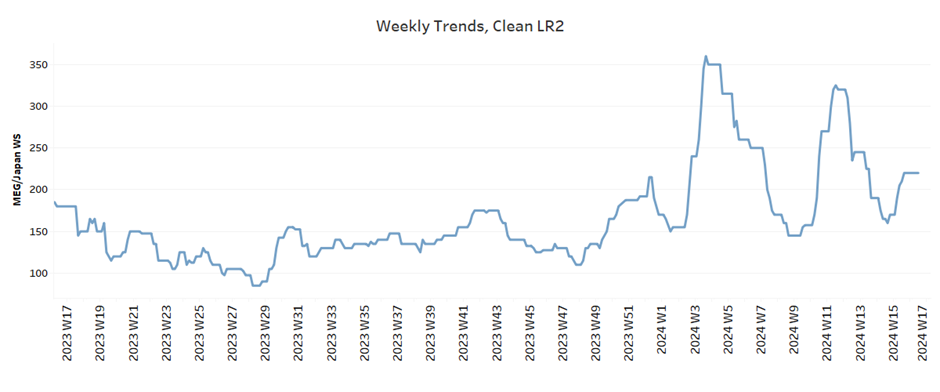

LR2 Firmer

LR2 AG freight rates sustained levels above WS200, currently standing 19% higher than during a comparable week a year ago.

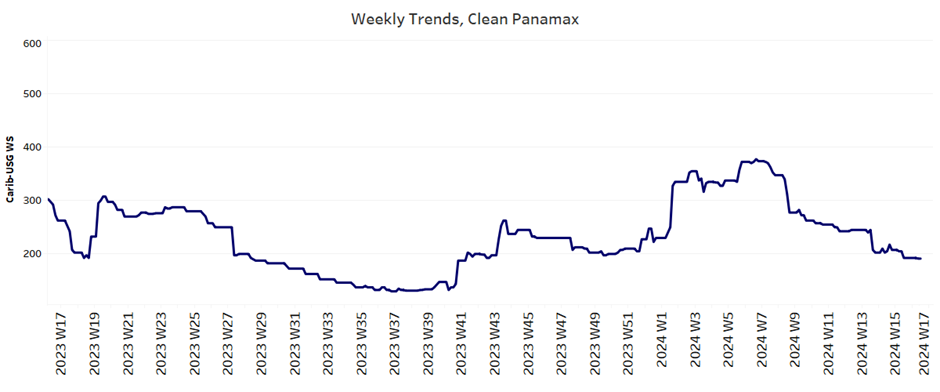

LR1 Weaker

Panamax Carib-to-USG rates have declined to 190WS, marking a 37% decrease compared to the rates observed during a comparable week a year ago.

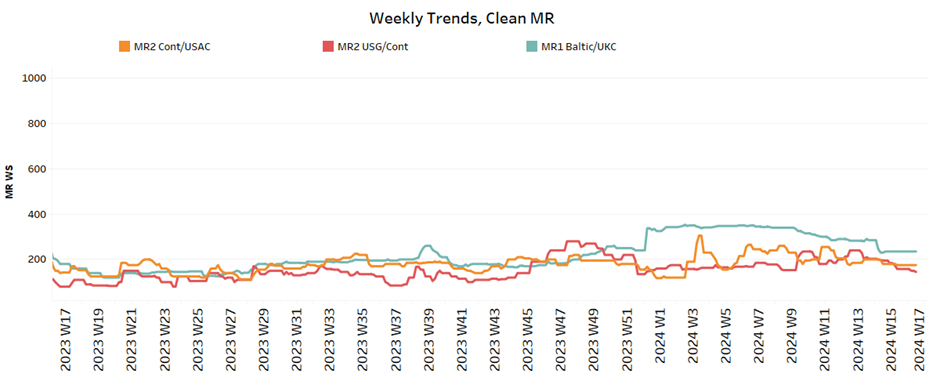

‘Clean’ MR Weaker

MR1 rates for shipments from the Baltic continent held a weakening trend, hovering around 230WS. Today's sentiment reflects a decrease of 15% from the rates observed a month ago. Meanwhile, MR2 rates for shipments from the continent to the USAC have plummeted to 175WS, marking a 15% decrease compared to rates observed a month ago.

SECTION 2/ SUPPLY

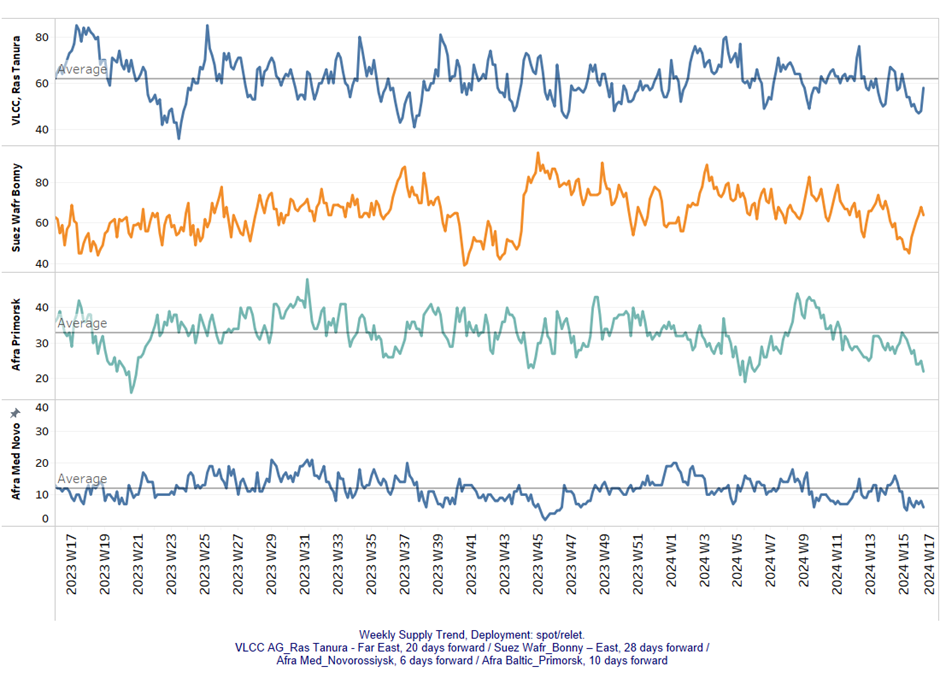

‘Dirty’ (# vessels) - Mixed

The supply trend for crude tankers is showing an upward trajectory in the VLCC Ras Tanura and Suez WAfr segments, while a downward trend appears to persist for the Aframax Med and Primosk segments.

VLCC Ras Tanura: The ship count has climbed to 58, edging closer to surpassing the annual average of 60. There are indications suggesting a potential upward revision by the end of the month, signalling a possible continuation of this upward trend.

Suezmax Wafr: The current ship count has exceeded 60, marking a reversal from the downward trend observed just two weeks ago.

Aframax Primorsk: The current ship count sustained levels below the annual average of 30 for the last four weeks, representing a nearly 30% decrease from the peak recorded during week 13.

Aframax Med Novo: The vessel count has persisted below the annual average of 10, indicating a continuing downward trend with signs pointing towards further decline until the end of the month.

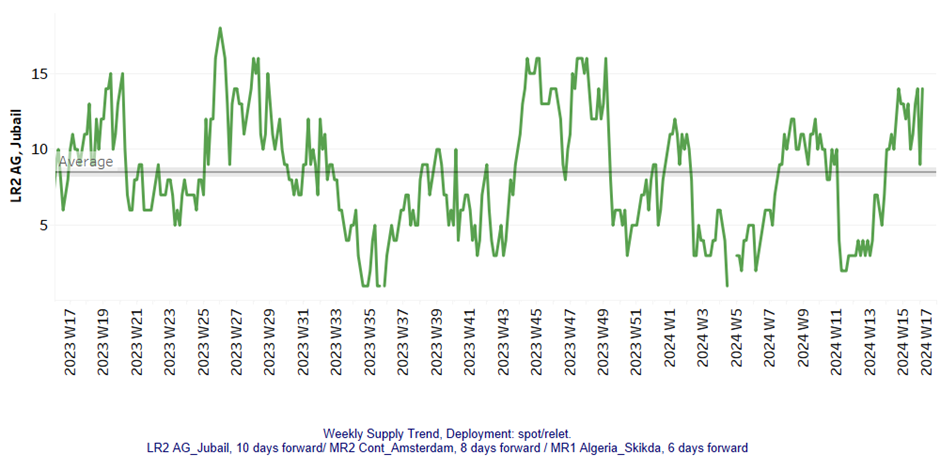

'Clean' LR2 (#vessels) - Increasing

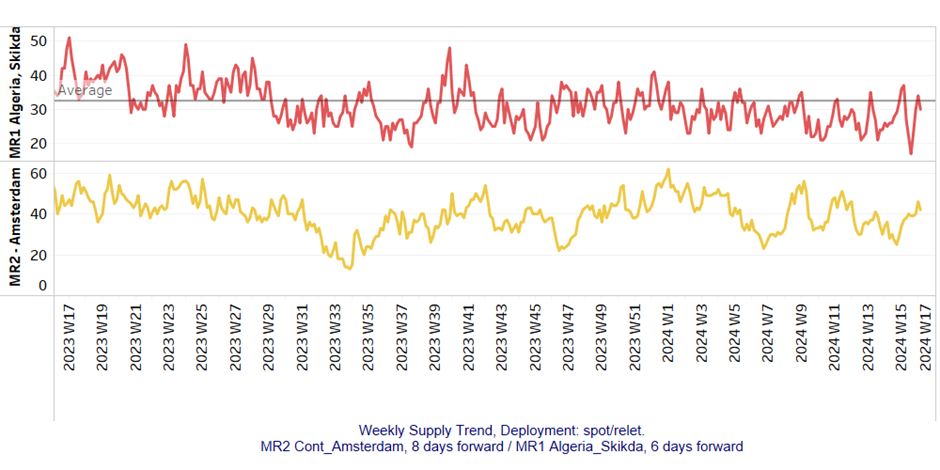

MR (#vessels) - Increasing

Clean LR2 AG Jubail: The upward trend has undergone a significant revision in the past two weeks, with current levels now surpassing the annual average of 10, reaching approximately 14. This surge has even eclipsed the previous high observed in week 9.

Clean MR: Vessel activity for MR1 at Algeria's Skikda port has surged to nearly match the annual average, with approximately 30 vessels recorded. Likewise, in MR2 Amsterdam, there has been a notable increase to 46 vessels, marking a significant rise from the low of 25 observed during week 13.

SECTION 3/ DEMAND (Tonne Days)

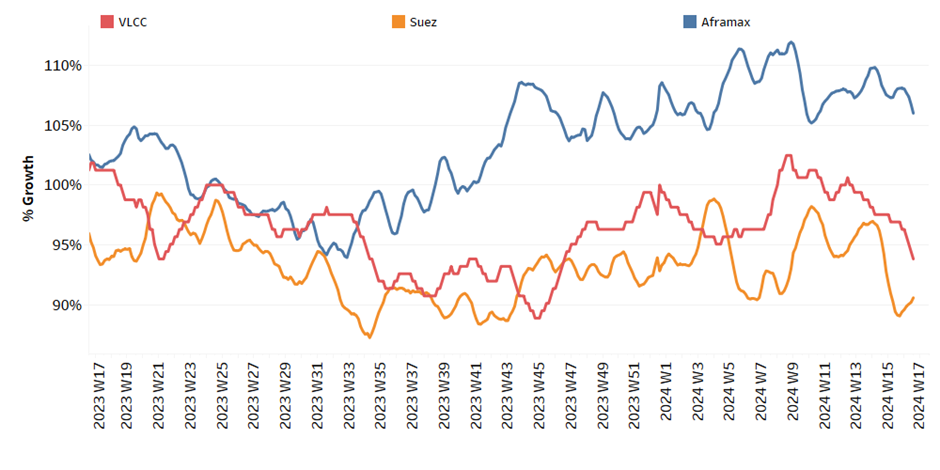

‘Dirty’ Decreasing

Dirty tonne days: April witnessed a downturn in the growth of dirty tonne days for VLCC, Suezmax, and Aframax vessels. However, there has been a recent slight uptick in the growth of dirty tonne days for the Suezmax category, although it remains to be seen if this will solidify into a sustained trend in early May.

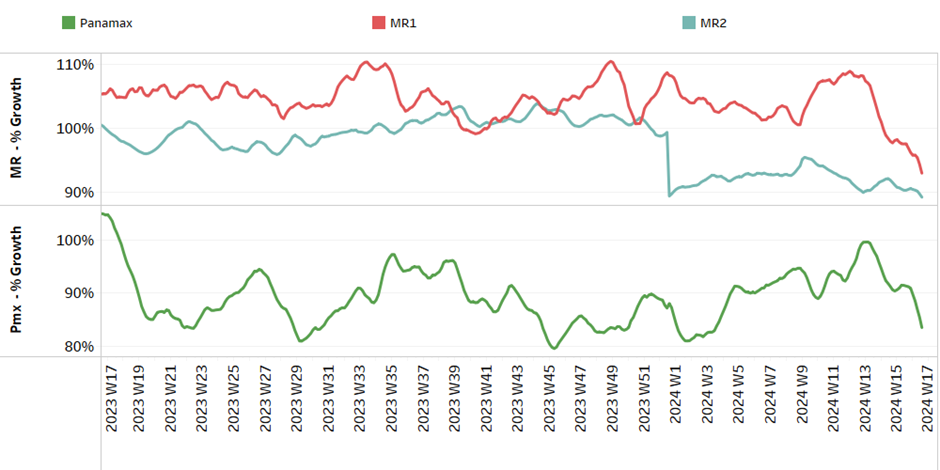

‘Clean’ Decreasing

Panamax tonne days: The final week of April solidified a significant decline in the growth of tonne days, making it increasingly challenging to achieve the levels observed during the peak in week 13 in the coming days.

Clean MR tonne days: The tonne-day growth for both MR1 and MR2 vessel sizes has shown a consistent downward trend over the past nine weeks, with no indications of an imminent upturn.

Similar Stories

Hormuz: IMO evacuation plan put on hold following ship attack until further notice