WorldACD Air cargo trends for the past 5 weeks (wk 1):

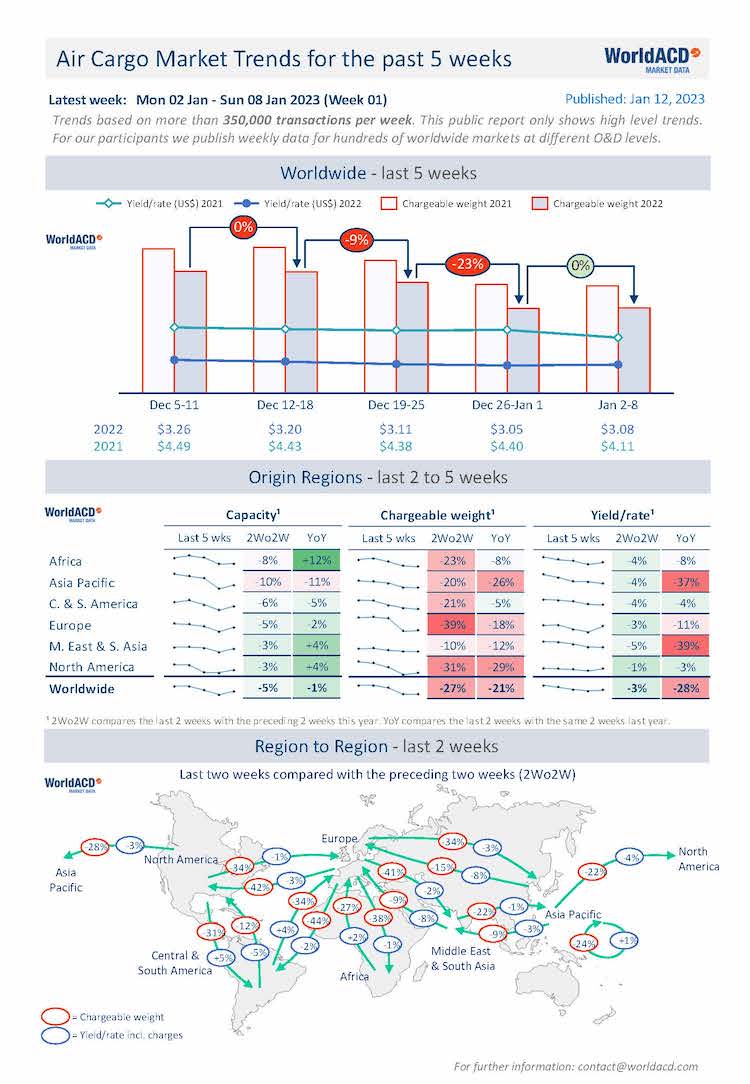

Jan 12, 2023Global air cargo tonnages have shown no sign yet of a post-holiday season recovery, whereas last year there was already an upswing by the end of the first week, the latest preliminary figures from WorldACD Market Data indicate, consistent with a continued softening of market conditions.

Figures for week 1 (2 to 8 January) show worldwide tonnages to be stable compared with the previous week, while last year in the same period an increase of +4% was observed. The underlying trend, therefore, seems to be a global weakening of demand. However, average rates held firm in the first week of 2023, showing an increase of +1% compared with the previous week, whereas last year a substantial decrease was recorded of -5%.

Comparing weeks 52 and 1 with the preceding two weeks (2Wo2W), tonnages decreased -27% below their combined total in weeks 50 and 51, with a -5% decrease in capacity, while average worldwide rates declined -3% – based on the more than 400,000 weekly transactions covered by WorldACD’s data.

In this two-week period, tonnages were significantly down between all regions, as is common this time of year. Notable decreases were recorded between Europe and Central & South America (-34% eastbound, -44% westbound), between Europe and North America (-34% eastbound, -42% westbound), between Europe and Africa (southbound

-38%, northbound -27%) and between Europe and Asia Pacific (-34% eastbound, -15% westbound).

Year-on-Year perspective

Comparing the overall global market with this time last year, chargeable weight in weeks 52 and 1 was down -21% compared with the equivalent period last year, at -1% lower capacity. Notably, tonnages ex-North America are down by -29%, and ex-Asia Pacific tonnages are -26% below their strong levels this time last year. But there were also double-digit percent year-on-year drops on tonnages outbound from Europe (-18%) and Middle East & South Asia (-12%).

Overall capacity has fallen slightly (-1%) compared to the previous year and is down from Asia Pacific (-11%), Central & South America (-5%) and Europe (-2%), whereas from Africa (+12%), North America (+4%) and Middle East & South Asia (+4%) capacity remains above its levels this time last year.

Worldwide rates are currently -28% below their unusually elevated levels this time last year at an average of US$3.08 per kilo in week 1, despite the effects of higher fuel surcharges, but they remain significantly above pre-Covid levels.

Similar Stories

Chapman Freeborn helps restore Air Zimbabwe’s Harare–London Gatwick route

View Article

Airfowarders Association regrets resumption of hostilities between United States and Iran

View Article

FlyUs expands Riyadh Cargo partnership

View Article

Chicago Rockford International Airport marks groundbreaking of 334,800-square-foot Hillwood logistics development

View ArticleCIRCLE Group signs a framework agreement for the Progressive Digital Development of a European Airport Cargo Ecosystem

CIRCLE Group announces the signing, through its subsidiary Cargo Start, of a framework agreement.

View Article

Amazon supports weekly humanitarian relief flights to Venezuela in first-of-its-kind collaboration

View ArticleGet the most up-to-date trending news!

SubscribeIndustry updates and weekly newsletter direct to your inbox!

Follow us on social media:

![]()

![]()