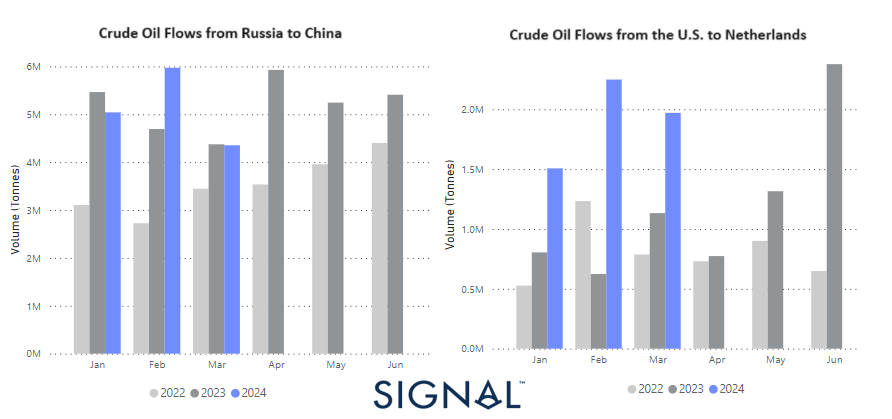

Chart of the Week: Dirty crude oil flows from Russia and U.S.Russia remained the key origin country for crude oil shipments to China, while the United States increased its volume of shipments to the Netherlands

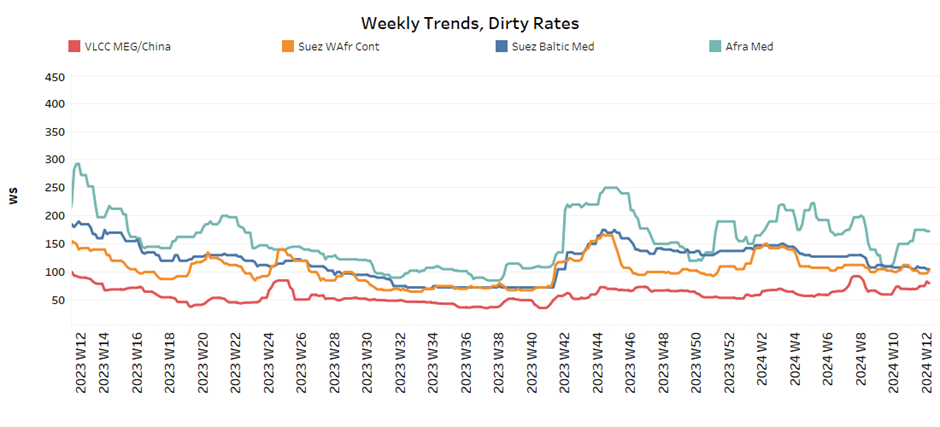

In the third week of March, there's a noticeable improvement in sentiment surrounding VLCC MEG-China rates, offering a glimmer of optimism. However, this comes against the backdrop of tonne days growth continuing to paint a picture of decreasing market conditions. In the Aframax Mediterranean region, market prices remained firm for another week, raising the possibility of reaching a new peak by month's end. Nevertheless, the freight market appears poised to grapple with ongoing instability, driven by the dwindling growth of dirty demand tonne days and the evolving supply trends in vessel activity, which could further influence market prices.On the front of dirty oil shipments, it's noteworthy that Russia maintains its status as a significant origin country for crude oil flows to China, while the United States has been bolstering the Netherlands' appetite with record monthly shipment volumes in the first quarter of the year. Meanwhile, in the realm of oil supply, the challenge posed by OPEC+ announcing an extension of oil production cuts through 2024 has prompted the IEA to revise its forecasts for crude oil and petroleum products in its March Short-Term Energy Outlook. Now, the IEA foresees a scenario with significantly less global oil production than world oil consumption in the first half of 2024, necessitating draws on world petroleum stocks.

For more information on this week's trends, see the analysis sections below:

In the third week of March, a glimmer of optimism emerged in the sentiment surrounding the VLCC MEG-China freight market, hinting at a potential uptick in momentum. Despite this, current market prices remain subdued, lingering at lower levels. Conversely, in the Aframax segment, Mediterranean rates are on an upward trajectory, steadily improving and surpassing previous lows witnessed during week 9, culminating in a new peak.

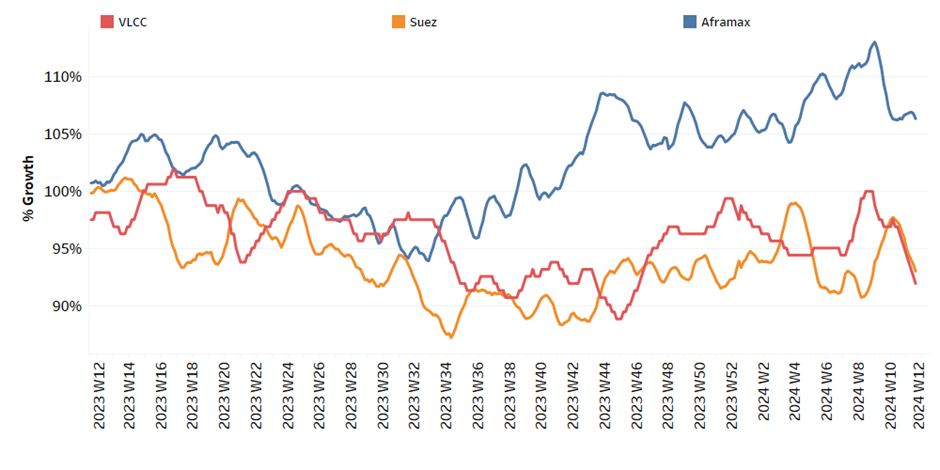

VLCC MEG-China freight rates stood at 74WS, marking a notable increase of almost 4 points compared to the previous week. However, they remain 15 points below the peak observed in mid-February.

Suezmax freight rates for shipments originating from West Africa to continental Europe have remained slightly above 100WS since the start of the month, signalling a year-on-year decline of 30%. Meanwhile, in the Suez Baltic Med route, rates persist in a downward trajectory, falling below the 100WS threshold, marking a significant 40% decrease compared to the previous year.

Aframax Med freight rates surged, maintaining the momentum of the previous week and exceeding 175WS. Nevertheless, current rates reflect a 23% decrease compared to the corresponding week from a year ago.

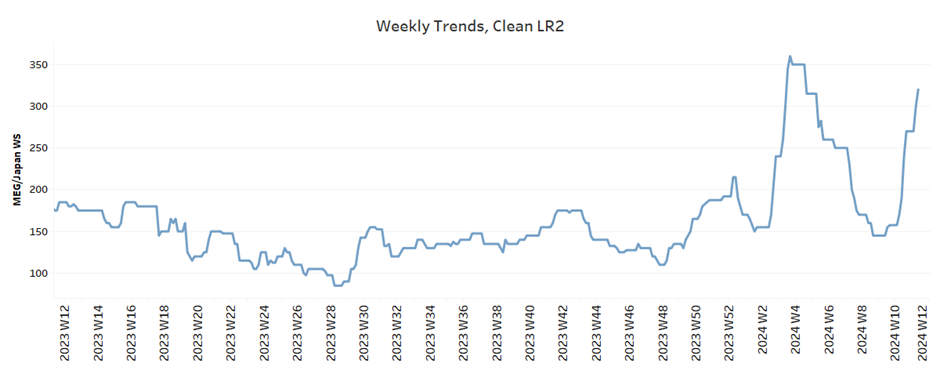

‘Product’ WS LR2 Firmer

LR2 AG freight rates have continued to soar, surpassing the previous weekly peak and reaching levels exceeding 300WS. This surge represents an astonishing increase of almost 60% compared to the levels observed during a comparable week just a month ago.

LR1Weaker

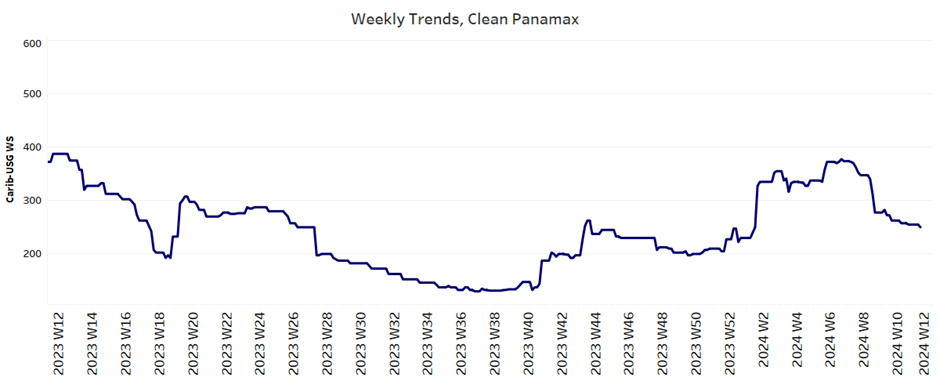

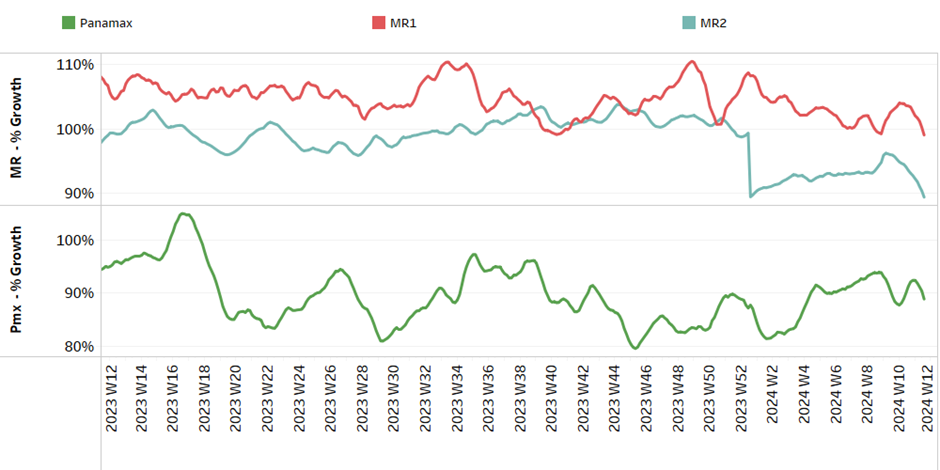

Panamax Carib-to-USG rates have declined to 250WS, marking a 33% decrease compared to the rates observed during a comparable week just a month ago.

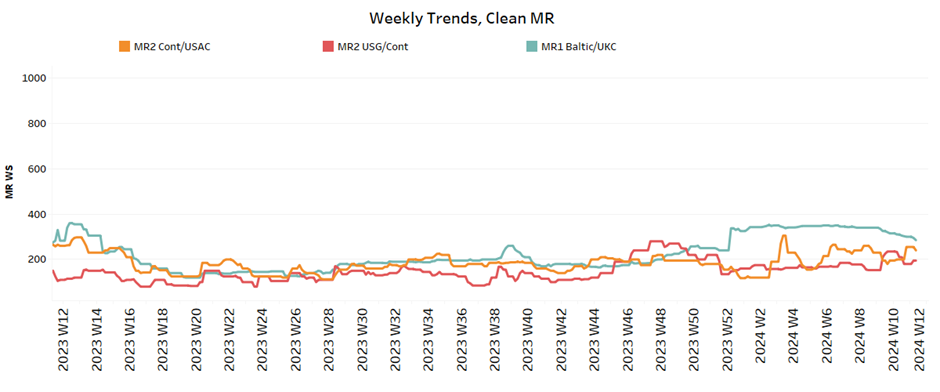

‘Clean’ MR Mixed

MR1 rates for shipments from the Baltic continent are currently hovering around 280WS, reflecting a decrease of 20% compared to the peak observed in mid-February. Meanwhile, MR2 rates for shipments from the continent to the USAC have risen above 200WS, marking a 20% increase compared to the previous week.

SECTION 2/ SUPPLY

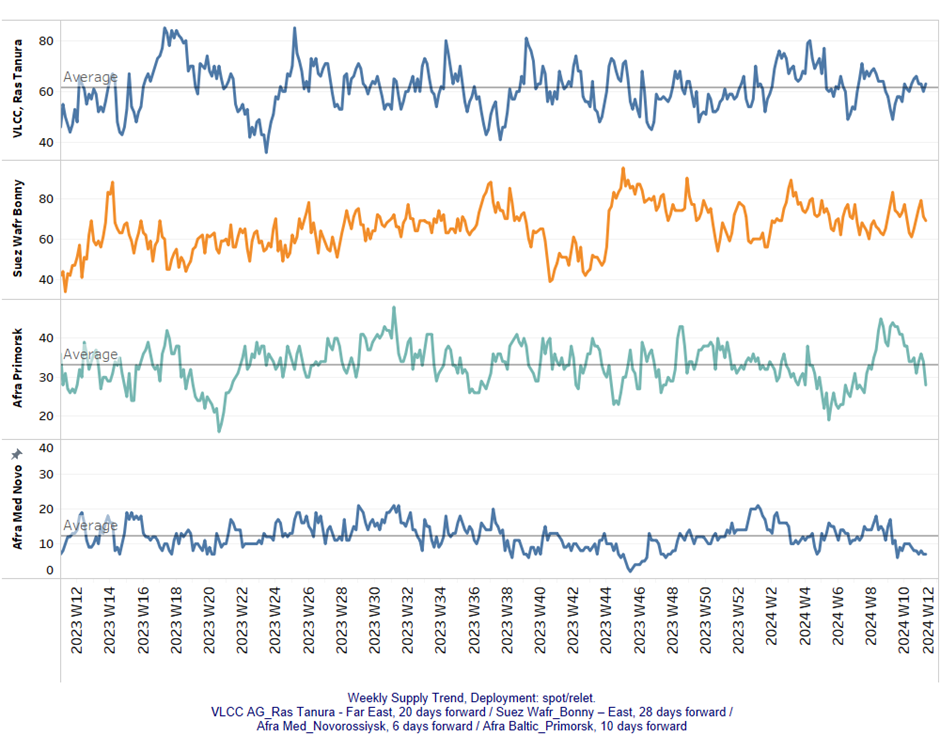

'Dirty' (#vessels) - Mixed

Recent indications point towards a continued decrease in the Aframax Primorsk and Med Novo markets. Conversely, in the VLCC Ras Tanura market, although there has been a recent uptick compared to the lows observed two weeks ago, current estimates suggest that rates have not yet surpassed the annual average.

VLCC Ras Tanura: The ship count held levels of the previous week at 60, defying estimates for surpassing the annual average.

Suezmax Wafr: The current ship count fell below 70, almost 7 less than the previous week, while recent indications provoke a downward trend for the end month.

Aframax Primorsk: The current number of ships has dropped to 28, which is 5 vessels lower than the annual average. Moreover, this recent decrease falls short of the peak of 40 ships recorded three weeks ago.

Aframax Med Novo: The number of vessels has consistently remained below the annual average of 10, signalling a decrease in activity since the end of week 10.

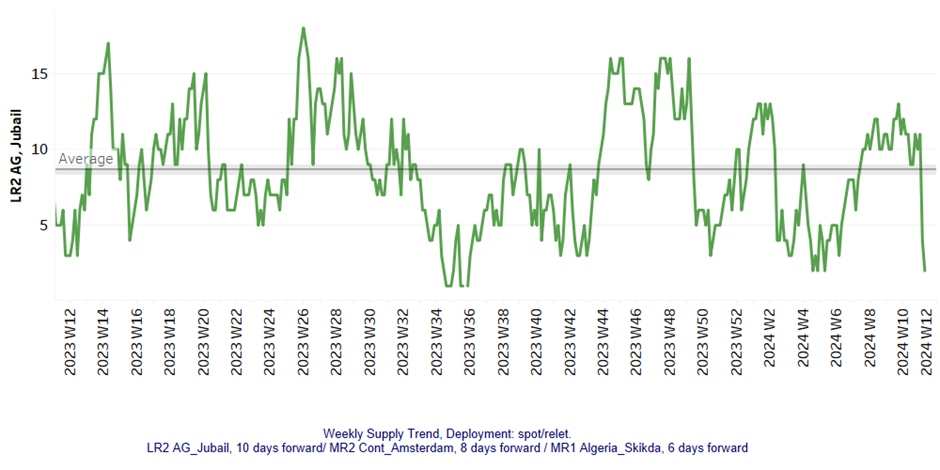

'Clean' LR2 (#vessels) - Decreasing

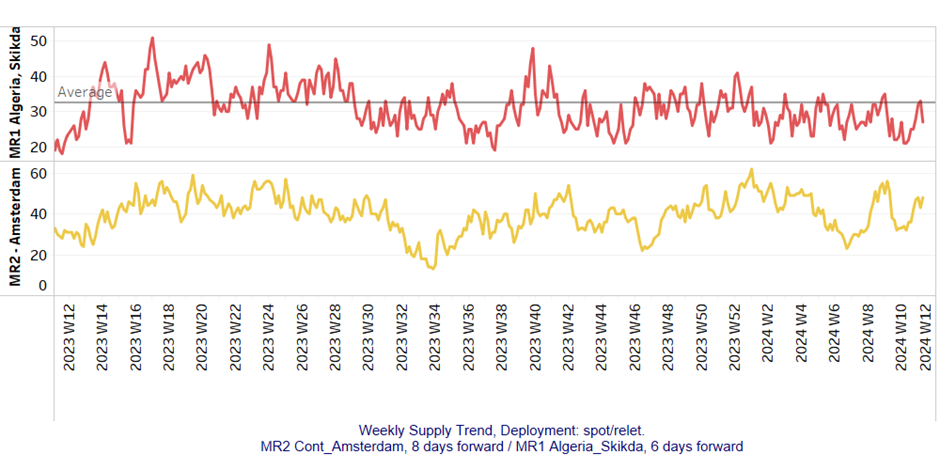

MR (#vessels) - Increasing

Clean LR2 AG Jubail: The downward trend observed in the previous two weeks has continued significantly, with current levels hovering at the lowest point recorded since week 4.

Clean MR: Vessel activity for MR1 in Algeria's Skikda port, while showing signs of an increase, still remains below the annual average, with vessel activity hovering around 27. Meanwhile, in MR2 Amsterdam, there has been a notable increase to 48 vessels, marking a rise of 16 compared to the previous week and edging closer to the peak observed four weeks ago.

SECTION 3/ DEMAND (Tonne Days)

‘Dirty’ Decreasing

Dirty tonne days: The downward trend has persisted since the beginning of the month. However, there are notable shifts in tonne days dynamics within different segments of the tanker market. In the VLCC segment, the growth trajectory now appears to mirror that of Suezmax vessels. Conversely, in the Aframax segment, it appears that the market has already hit its low point, with a consistent pace of percentage growth observed over the last two weeks.

‘Clean’ Decreasing

Panamax tonne days: The third week of March has once again brought a return to a downward trend, following a brief period of firmer growth observed in the previous week. Additionally, it appears that the recent level of growth has plateaued, resembling the rates recorded four weeks ago.

Clean MR tonne days: The tonne-day growth for both MR1 and MR2 vessel sizes is now unmistakably trending downward, with MR1 experiencing a more pronounced decline compared to MR2.

Similar Stories

Port of Los Angeles’ Seroka report 1 million TEUs in June up 12%