WorldACD Weekly Air Cargo Trends (week 21) - 2025

Jun 03, 2025The air cargo market was stable in terms of tonnage on a worldwide level in the week ending Sunday, May 25 (week 21), compared to the previous week. Although the week-on-week worldwide figure remained flat, demand was 6% higher than last year, with the largest absolute volume growth in the Asia Pacific region. Thanks to the strong increase in week 20, the last two weeks taken together were up with a high single digit (+7%) compared to the two weeks before combined (2Wo2W), according to the latest data from WorldACD.

Zooming in on origin regions, different regional dynamics reveal a more nuanced picture in the last two weeks. Compared with the previous two weeks combined, the most buoyant region-to-region markets were Asia Pacific to North America (+19%) and North America to Asia Pacific (+13%), with the largest decline in volume from Central & South America to North America (-23%), which is a normal post-Mother’s Day flower shipments pattern.

Tonnages on China to USA lane recover as China to Europe expands

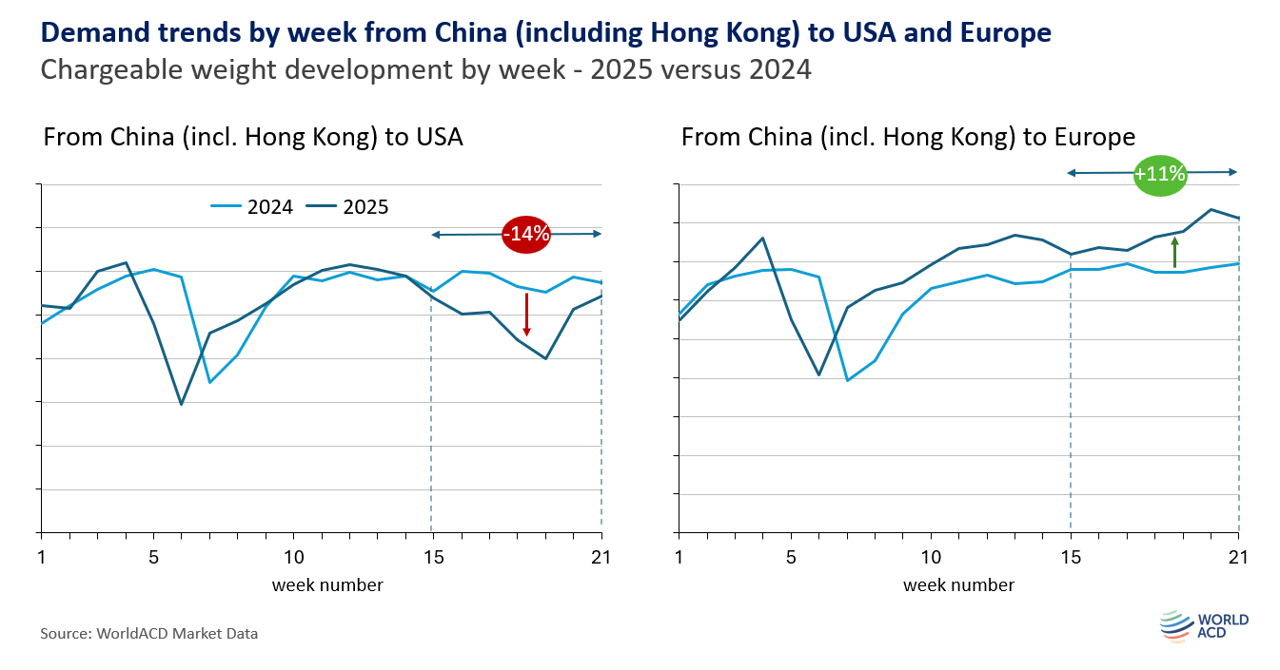

In the turbulent geopolitical climate all eyes are on what is happening from the air freight powerhouse China (including Hong Kong). With the air cargo industry flocking to the conference in Munich next week, this will be one of the most talked about topics. We share the most recent trends on the headhaul markets China to USA and Europe in the charts below. These show weekly demand trends for air cargo shipments from China to USA (left) and to Europe (right). The data include up to week 21, ending last Sunday, May 25.

Tonnages on China to USA lane recover as China to Europe expands

In the turbulent geopolitical climate all eyes are on what is happening from the air freight powerhouse China (including Hong Kong). With the air cargo industry flocking to the conference in Munich next week, this will be one of the most talked about topics. We share the most recent trends on the headhaul markets China to USA and Europe in the charts below. These show weekly demand trends for air cargo shipments from China to USA (left) and to Europe (right). The data include up to week 21, ending last Sunday, May 25.

For the last six-week period we observe the following:

- Air cargo exports from China to USA dropped by -14% compared with the same period in 2024. After the large drop in week 18 and 19, chargeable weight in week 21 was almost back at the level in 2024, with a -5% difference.

- Air cargo exports from China to Europe increased by +11% over the same time frame. Even though there was a modest week-on-week drop of -3% in week 21, we see that this market is increasingly showing higher volumes than in 2024.

Due to public holidays, this week’s trends publication is shorter than usual.

Similar Stories

Realterm and SARAA forge strategic partnership to deliver new state-of-the-art cargo facility at Harrisburg International Airport

View Article

Weekly Air Cargo Trends – June 22 to 28, 2026

View Article

Airforwarders Association issues new IATA framework forwarder risk warning on new IATA air waybill

View Article

Unilode launches Fire Containment Cover Leasing Solutions - expanding flexible safety support for airlines

View ArticleBreeze encourages freight forwarders to review insurance

Freight forwarders should take the opportunity to review their contractual arrangements and insurance protection, according to digital cargo insurance provider Breeze.

View Article

Soaring AI shipments invigorate air cargo’s resilience as global demand rises +7% in June

View ArticleGet the most up-to-date trending news!

SubscribeIndustry updates and weekly newsletter direct to your inbox!

Follow us on social media:

![]()

![]()