WorldACD Air cargo trends for the past 5 weeks (wk 45):

Nov 21, 2022There are still no signs of any fourth-quarter (Q4) seasonal uplift in air cargo demand or pricing, with the downward trend of the last several months continuing into the second week of November – when peak season is usually in full flow.

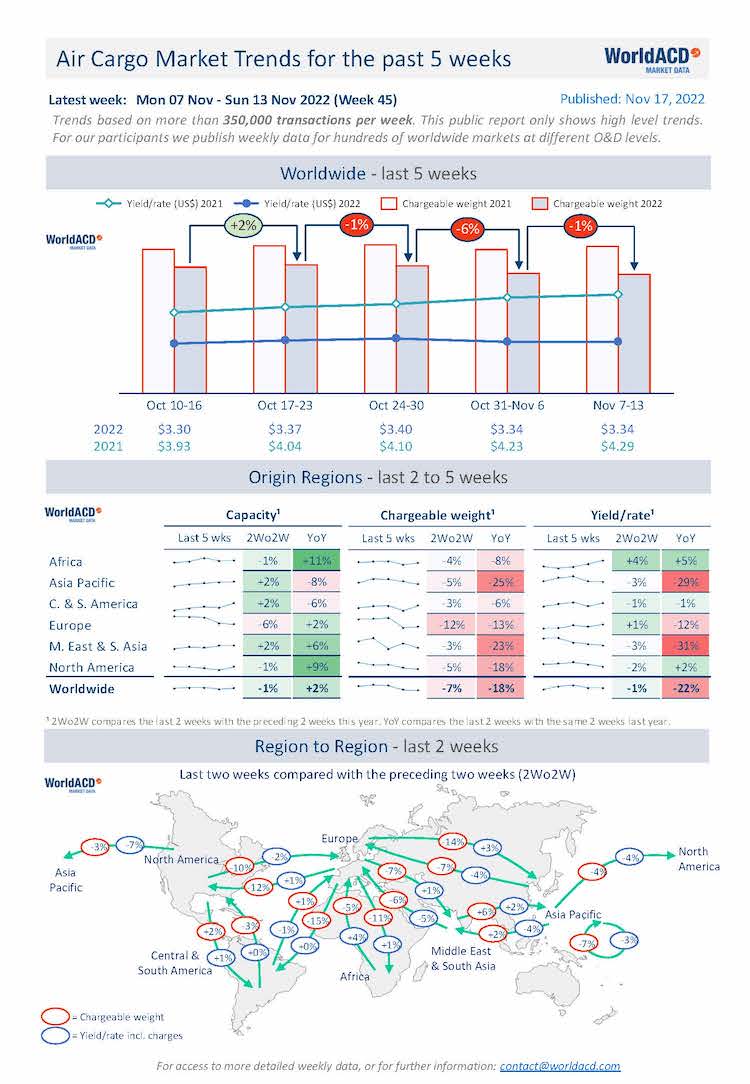

Following a steep decline in the week to 6 November (week 44), reported by WorldACD last week, the latest preliminary figures from WorldACD Market Data show that weakening trend continue in this week’s report – although the drop was less steep on a week-over-week basis.

Figures for week 45 (7 to 13 November) show a further -1% drop in worldwide flown tonnages from the previous week, and a stable average price. But comparing weeks 44 and 45 with the preceding two weeks (2Wo2W), tonnages were -7% below their level in weeks 42 and 43, while average worldwide rates decreased by -1%, in a decreasing capacity environment (-1%) – based on the more than 350,000 weekly transactions covered by WorldACD’s data.

Across that two-week period, outbound tonnages dropped from all the main regions, most notably ex-Europe (-12%), ex-Asia Pacific (-5%) and ex-North America (-5%). On a lane-by-lane basis, strong decreases were recorded between Europe and North America (-12% westbound and -10% eastbound) and between Europe and Asia Pacific

(-7% westbound and -14% eastbound).

There were also double-digit percentage drops in tonnages from Europe to Central & South America (-15%) and to Africa (-11%), while intra-Asia Pacific volumes fell by

-7%. Chargeable weight growth outbound from Middle East & South Asia to Asia Pacific was the only significant positive exception (+6%), on a 2Wo2W basis.

Year-on-Year Perspective

Comparing the overall global market with this time last year, chargeable weight in weeks 44 and 45 was down -18% compared with the equivalent period in 2021, despite a capacity increase of +2%. Notably, tonnages ex-Asia Pacific are -25% below their strong levels this time last year, and Middle East & South Asia origin tonnages are -23% below last year. But there were also double-digit percentage year-on-year drops outbound from both North America (-18%) and Europe (-13%), despite higher capacity.

Capacity from all the main origin regions, with the exception of Asia Pacific (-8%) and Central & South America (-6%), is (significantly) above its levels this time last year: North America +9%, Middle East & South Asia +6%, Europe +2% and a double-digit percentage rise from Africa (+11%).

Worldwide rates are currently -22% below their levels this time last year at an average of US$3.34 per kilo, despite the effects of higher fuel surcharges, but they remain significantly above pre-Covid levels.

Similar Stories

Realterm and SARAA forge strategic partnership to deliver new state-of-the-art cargo facility at Harrisburg International Airport

View Article

Weekly Air Cargo Trends – June 22 to 28, 2026

View Article

Airforwarders Association issues new IATA framework forwarder risk warning on new IATA air waybill

View Article

Unilode launches Fire Containment Cover Leasing Solutions - expanding flexible safety support for airlines

View ArticleBreeze encourages freight forwarders to review insurance

Freight forwarders should take the opportunity to review their contractual arrangements and insurance protection, according to digital cargo insurance provider Breeze.

View Article

Soaring AI shipments invigorate air cargo’s resilience as global demand rises +7% in June

View ArticleGet the most up-to-date trending news!

SubscribeIndustry updates and weekly newsletter direct to your inbox!

Follow us on social media:

![]()

![]()