Offshore wind expenditure set to match upstream oil and gas in Europe in 2021, surpass it in 2022

Jun 08, 2020The oil market collapse caused by the Covid-19 pandemic is set to delay several oil and gas developments in Western Europe, putting capital expenditure in the offshore sector on a continued downwards trajectory through 2022.

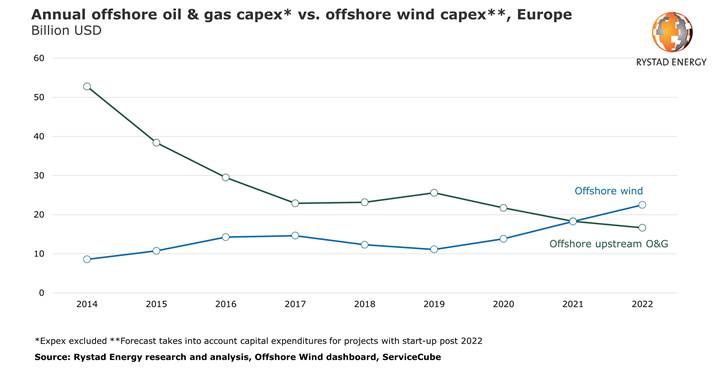

In light of the postponement of multiple final investment decisions (FIDs) on projects and lower investments in offshore oil and gas, coupled with increasing activity in the offshore wind sector, Rystad Energy expects that the two markets will reach parity as soon as next year. We anticipate that capital expenditure (capex) on offshore wind will surpass upstream O&G spending in Europe in 2022.

Capex towards offshore wind in Europe surpassed the $10 billion mark in 2015 and has since hovered in the range of $10 billion to $15 billion per year. Annual capex levels are expected to rise from around $11.1 billion in 2019 to around $13.8 billion in 2020, $18.2 billion in 2021 and more than $22 billion in 2022.

The abundant oil supply and reduced demand have taken their toll on the oil price, and consequently annual capex towards upstream offshore oil and gas in Europe is expected to decline from more than $25 billion in 2019 to less than $17 billion in 2022.

“Offshore wind development in Europe is expected to flourish in the coming years as countries strive to reach their ambitious 2030-targets – and large investments will be required,” says Alexander Flotre, Rystad Energy’s project manager for offshore wind.

“Commissioning activity is expected to increase towards 2025, and projects expected to be operational in 2023-2025 are already driving up capital expenditure in 2020. This trend will continue in the coming years,” Flotre adds.

Historically, Europe has been the key market for offshore wind development, accounting for almost 80% of global installed capacity at the end of 2019. While strong growth is expected in China, South East Asia and the US in the years to come, Europe is expected to maintain its number one position through 2025 in terms installed capacity.

From an installed base of 21.9 gigawatts (GW) in 2019, European capacity is expected to increase to more than 53 GW by 2025, constituting an annual growth rate of 16%. While Europe’s ambitious plans for 2030 will require new tender rounds in the coming years, most of the commissioning activity towards 2025 is expected to come from projects that have already been approved.

The UK is the largest country in Europe in terms of offshore wind capacity and is expected to drive a big portion of the growth towards 2025, with mega-projects such as Dogger Bank, Sofia and additional Hornsea phases currently on the cards, among others. Other established countries such as the Netherlands, Germany, Belgium and Denmark are also expected to contribute to the increased spending levels, while newcomers such as France and Poland will add to the growth in the 2023 to 2025 period.

“Many service companies have already transitioned towards concentrating increasingly on offshore wind activities, compared to their legacy oil and gas business. For these players, the growth in the offshore wind market provides a well-timed cushion that softens the blow of declining investments in the traditional oilfield services sector,“ Flotre concludes.

Similar Stories

AFC deepens Angolan investment drive as Angola Oil & Gas (AOG) 2026 Elite Sponsor

Africa Finance Corporation (AFC) is expanding its role in Angola's energy and infrastructure sectors.

View Article

Hybrid sales rise while battery electric sales remain lower after tax credit expiration

View ArticleKBR selected by Power2X as project management consultant for its eFuels project in Rotterdam

KBR announced it has been awarded the Project Management Consultant (PMC) contract by Power2X for its eFuels project in Rotterdam.

View Article

The Port of Barcelona increased traffic by 3.5% in the first half of the year

View ArticleWhy Venezuela’s energy reforms are bringing investors back to the table in London

With Venezuela introducing sweeping reforms to its hydrocarbons sector and renewed international interest gathering pace, the Venezuela Energy Week London Industry Showcase will bring together policymakers, investors and industry leaders.

View Article

CN delivers on commitments with strong second quarter results

View ArticleGet the most up-to-date trending news!

SubscribeIndustry updates and weekly newsletter direct to your inbox!

Follow us on social media:

![]()

![]()