Global OFS demand is set for a 25% decline in 2020. Here is how the recovery will unfold

Jun 18, 2020Global demand for oilfield services (OFS), measured in the total value of exploration and production (E&P) company purchases, is set for a massive 25% yearly drop in 2020 as a result of the Covid-19-caused downturn, a Rystad Energy analysis shows. Spending is expected at $481 billion this year and take the first step on the road to recovery in 2021, when it is forecast to tick up by just about 2%.

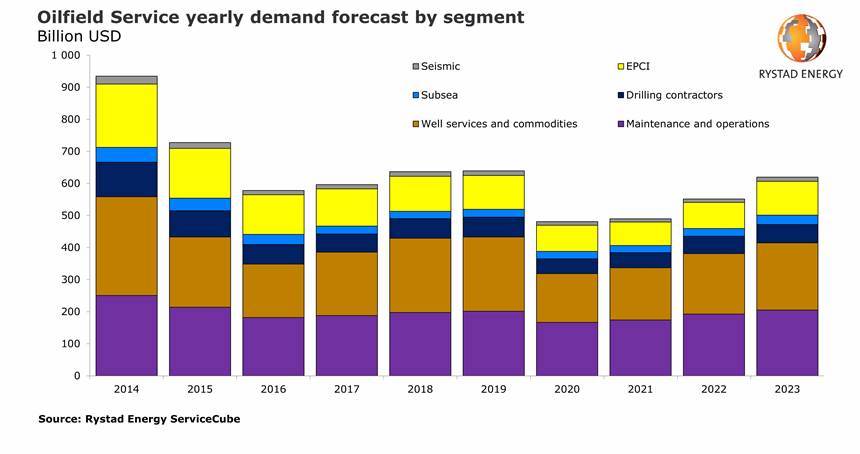

The recovery will accelerate further in 2022 and 2023, with OFS spending by E&Ps reaching some $552 billion and $620 billion, respectively. Despite the boost, purchases will not return to the pre-Covid-19 levels of $639 billion achieved in 2019.

The comeback will not be visible across all OFS segments from 2021, however. Well services and the pressure pumping market will be the first to see a boost, while other markets will need to get further depressed before recovering.

“Despite the recovery in oil prices, it will take many quarters before all segments of the supply chain see their revenues deliver consistent growth. In case of an upturn, operators would prefer flexible budget items with production increments and high-return investments with short pay-back times. Therefore, we expect well service segments to be the first to recover, while long-lead segments will pick up much later,“ says Rystad Energy’s Head of Energy Research Audun Martinsen.

Dividing OFS into six segments – maintenance and operations, well services and commodities, drilling contractors, subsea, EPCI and seismic – only the first three will manage to rise in 2021, while the latter three will have to brace for another year of falling revenues before they can expect improvements.

In absolute numbers, the maintenance and operations segment is poised for consecutive yearly rises in the next three years after slumping to $167 billion this year from $202 billion in 2019. We expect spending in this segment to recover to $175 billion in 2021, $193 billion in 2022 and $205 billion in 2023).

The well services and commodities segment is set for a similar recovery, but only after slumping to $152 billion in 2020 from $231 billion last year – the biggest decline among segments in absolute numbers. Here we see spending at $163 billion in 2021, $189 billion in 2022 and $210 billion in 2023.

The same pattern also applies to drilling contractors, with the segment falling to $46 billion in 2020 from $62 billion last year, and then rising to $47 billion in 2021, $54 billion in 2022 and $57 billion in 2023.

The subsea segment, on the other hand, will fall from $25 billion in 2019 to $24 billion in 2020 and decline further to $22 billion in 2021 – before starting to rebound to $24 billion in 2022 and to $29 billion in 2023.

Similarly, EPCI is set to fall to $81 billion in 2020 from $105 billion last year. It will slide further to $74 billion in 2021, before rising back to $81 billion in 2022 and growing to $106 billion a year later.

Lastly, seismic is poised to decline to $12 billion in 2020 from $15 billion in 2019. It will first keep dropping to $10 billion in 2021, before rebounding to $11 billion in 2022 and to $13 billion a year later.

“At best there will only be certain regions and service segments that will see their revenues grow consistently. For the whole supply chain to recover, we will likely need to wait until after 2023, when we expect service purchases to return to their 2019 levels,“ adds Martinsen.

Suppliers will face a continued challenge turning their bottom lines back into black and deal with their debt. However, while the oil and gas market is expected to take years to recover, the impending energy transition could be a potential avenue of hope as it could open up new markets for OFS players to leverage their capabilities and grow.

Similar Stories

CAMIMPEG confirmed as National Sponsor of Venezuela Energy Week 2026

CAMIMPEG has been confirmed as a National Sponsor of Venezuela Energy Week, taking place from October 26–29, 2026, in Caracas.

View ArticleHow the US-Iran scenarios shape Brent prices - Rystad Energy’s Oil Market Update

The oil market is shifting rapidly away from the simple question of whether the Strait of Hormuz reopens.

View Article

Port of Long Beach, MARAD sign first-of-its-kind partnership agreement on nuclear energy in maritime

View Article

DOT and Port of Long Beach sign agreement to test nuclear-powered vessels

View ArticleSPIRO publishes its first Sustainability Report

SPIRO published its inaugural Sustainability Report.

View Article

Latest Bureau Veritas approvals strengthen confidence in Anemoi Rotor Sail technology

View ArticleGet the most up-to-date trending news!

SubscribeIndustry updates and weekly newsletter direct to your inbox!

Follow us on social media:

![]()

![]()