Global demand for natural gas will drop 2% in 2020 as Covid-19 lockdowns take toll

May 18, 2020Commercial and industrial demand for natural gas is declining as most countries around the world impose lockdowns to limit the spread of the Covid-19 pandemic. Rystad Energy estimates global natural gas demand to fall by almost 2% this year as a result of the lower activity.

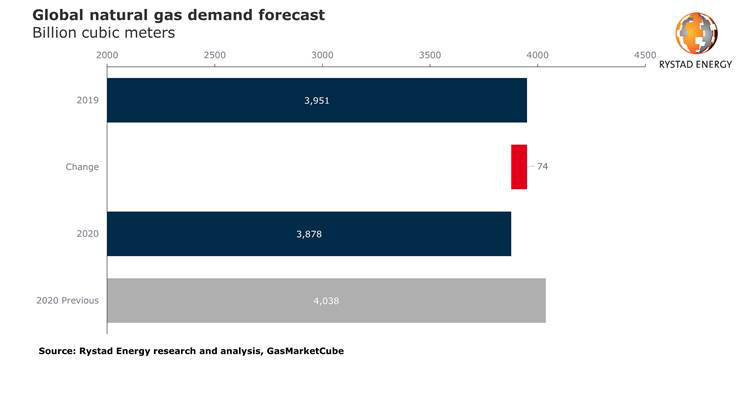

In absolute terms, we expect global gas demand to total close to 3,878 billion cubic meters (Bcm) in 2020, down from 3,951 Bcm last year. In our pre-Covid-19 estimates, this year’s natural gas demand was expected to grow to 4,038 Bcm.

Like oil demand, gas demand is also expected to suffer as a result of the slowdown. However, low prices are shielding gas demand to some extent as the fuel remains more competitive than other sources of energy, especially in the power sector where gas use remains relatively stable in most countries.

“2020 will be the first year since 2009 where there will be no growth in consumption. This will be a hard blow for an industry accustomed to yearly growth rates of more than 3%,” says Rystad Energy’s Head of Gas and Power Markets Carlos Torres-Diaz.

The impact on gas demand has varied substantially from country to country depending on the severity of lockdown measures and factors such as the power mix and industrial activity. Countries with capacity to switch from coal to gas will see less effect from the demand drop.

Italy is one of the countries that have been the most affected by Covid-19, and as a result the government decided to impose a strict lockdown starting in the beginning of March. The average loss in gas demand from the power and industrial sectors has been a staggering 23% over the duration of the lockdown. However, Italy has little coal-power generation capacity, meaning that any reduction in power demand will represent a similar drop in gas-for-power demand as a it is difficult to achieve a reduction in generation from renewable sources.

Other European countries have seen similar effects, with the International Energy Agency estimating a total loss in weather-adjusted gas demand of 25% in France and 19% in the UK.

On the other hand, demand in the US continues to thrive, mostly as a result of increasing demand from the power sector which has compensated for the drop in other sectors. Gas demand from the power sector has averaged 25 billion cubic feet per day (708 million cubic meters per day) over the last two weeks, which is practically in line with last year’s level.

But there have been periods during the current lockdown where demand has been more than 15% above last year’s level. The main reason for this is that gas prices remain very low, and while coal prices have also dropped, gas is still more competitive in power generation. The drop in US power demand has therefore pushed coal out of the generation stack rather than gas.

There are many other countries that also have a large coal-to-gas switching capacity, such as Australia, Germany and South Korea, which could see similar demand responses to the one seen in the US.

A lot of uncertainty remains about the actual impact on gas demand. The possibility of new lockdowns, the slowdown in economic growth and the effect of stimulus packages on reactivating commercial and industrial activity could all tip the gas-demand scale.

This uncertainty represents a downside risk for gas demand for the rest of the year. However, Rystad Energy has forecasted natural gas production to be around 4,000 Bcm in 2020 based on the lower investment activity expected across the E&P industry during this year.

Given that global gas storage capacity is very limited and that a lot of the gas production is driven by liquids, producers will push these volumes into the market. This could trigger a demand response to absorb the additional volumes, but this will be very dependent on gas prices remaining competitive to coal. Our forecast is for European gas prices (TTF) to average $3.3 per MMBtu and Asian spot prices to average $3.8 per MMBtu this year, which is below the coal-to-gas switching range in most countries.

Therefore, if coal producers manage to reduce prices further and the steep contango in the gas forward curves remains, then there is a risk of seeing a slowdown in gas demand towards the end of the year.

Similar Stories

CORE POWER, Maersk, LR and the Port of Rotterdam publish study on port calls for nuclear ships

View Article

Cadeler completes final turbine installation at Sofia Offshore Wind Farm

View Article

Largest wind farm in the United States starts commercial operations

View Article

Fraport Traffic Figures – May 2026: Frankfurt back on passenger growth track

View Article

Signal Ocean: South Asian demand keeps pushing coal flows higher

View Article

Higher blending targets drive RIN prices close to record highs

View ArticleGet the most up-to-date trending news!

SubscribeIndustry updates and weekly newsletter direct to your inbox!

Follow us on social media:

![]()

![]()

![[Freightos Weekly Update] Ocean rates climbing, with more increases expected soon](https://www.ajot.com/images/uploads/article/_thumbs/Support_grows_for_India%E2%80%99s_new_maritime_CCTV_rules.jpg)